Questions Remain on the Enhanced Employee Retention Credit (ERC) – We Offer Some Answers

The “Consolidated Appropriations Act, 2021” (“CAA”) provides relief to individuals, businesses, health care providers, and others impacted by the COVID-19 pandemic. A key opportunity for businesses in the CAA is an expansion of the “Employee Retention Credit” (“ERC”), which was first established in the CARES Act. While the CAA made several enhancements to the ERC, it left employers with many questions. Below, we answer some of those questions:

Get answers directly from a tax expert here:

1. What Businesses (Employers) are Eligible for the ERC?

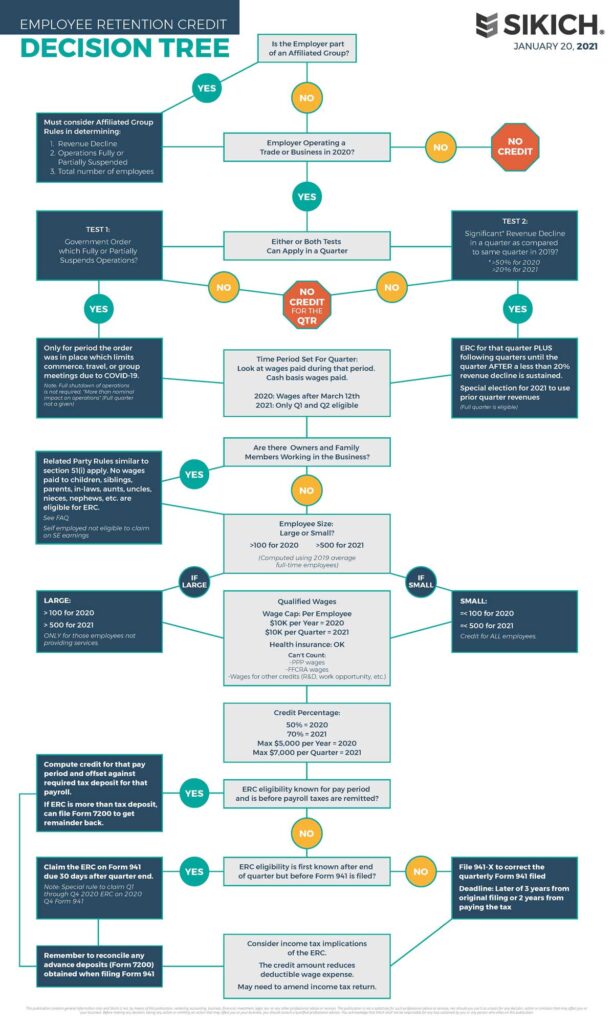

The organization must be carrying on a trade or business in 2020 and meet one of the following two criteria:

- Full or Partial Suspension Due to Government Order

- Significant Decline in Gross Receipts (see below)

2. What is a “Significant Decline” in Gross Receipts?

For 2020 ERC, the quarterly revenue decline needs to be more than 50%. To determine this, employers would compute their 2020 quarterly revenue and compare it to the same quarter for 2019.

For 2021 ERC, the quarterly revenue decline needs to be more than 20%. Employers would compare their 2021 quarterly revenue to the same quarter for 2019.

A special rule for 2021 ERC allows the business to look to the previous quarter to determine a revenue decline greater than 20%. For example, during the first quarter of 2021, the fourth quarter revenue of the previous year could be used (Quarter 4 of 2020 vs. Quarter 4 of 2019). This special rule would be used if Quarter 1 2021 revenues had not declined more than 20% from Quarter 1 2019 revenues.

For a business that started in 2019, the quarter the business began should be the base of determining the quarterly decline, until the business reaches a year of operations. For example, a new business that started in the second quarter of 2019 would use that quarter as the base to determine revenue decline for either first quarter 2020 or second quarter 2020. If a business started in the middle of a quarter in 2019, an estimate of that period’s gross receipts can be used.

3. Over What Period can a Business Claim the ERC?

The period depends on whether the business qualifies under the full or partial suspension of operations or from a revenue decline.

Partial or Full Suspension of Operations: For the period that the full or partial shutdown was in effect.

Revenue Decline: For the entire quarter, which first sustained the significant decline in gross receipts (“initial quarter”), and for at least the following quarter (“subsequent quarter”). Therefore, at least two quarters of wages will be able to be claimed. Note: it is only when a “subsequent quarter’s” revenues are more than 80% of the previous year that the ERC would not be available for the NEXT quarter.

Note: Affiliation rules are applicable to determine this revenue decline.

Example – Partial or Full Suspension of Operations:

A dentist was ordered to only be open for emergency care starting March 23, 2020 through May 17, 2020. Therefore, wages paid from March 23, 2020 to March 31, 2020 (a portion of the first quarter) and wages paid from April 1, 2020 through May 17, 2020 (a portion of the second quarter) would be eligible for the ERC. (For this example, we are assuming the facts and circumstances indicate that the dentist’s operations were not considered to be partially suspended AFTER the office reopened). The entire first quarter and second quarter wages paid would not be eligible.

Example – Revenue Decline:

If the same dentist above suffered a more than 50% decline in its second quarter 2020 revenues compared to 2019, the entire second quarter wages would be eligible. Although, the dentist could begin seeing regular patients on May 18, 2020, so the quarterly revenue decline causes the entire quarter’s wages to be eligible. In addition, because of the second quarter decline, the dentist would automatically be eligible for the ERC in the third quarter. Only if third quarter revenues were down less than 20% from third quarter 2019, would the dentist be ineligible for ERC starting the fourth quarter.

The following two examples further illustrate how the ERC revenue decline works:

- Q2 2019 = $100,000

- Q3 2019 = $100,000

- Q4 2019 = $100,000

- Q2 2020 = $45,000

- Q3 2020 = $75,000

- Q4 2020 = $81,000

- ERC for this quarter

- ERC for this quarter

- ERC for this quarter

In Example 1, second quarter revenues have declined more than 50% as compared to 2019, so it is eligible for ERC for the second quarter. The third quarter revenues recovered, but the decline was still 25% as compared to 2019. Because the third quarter revenue decline was more than 20%, the business will be eligible for the ERC in the fourth quarter. Note: in the above example, fourth quarter 2020 revenues could have been $100,000 with the same result: ERC is able to be claimed for the fourth quarter.

- Q2 2019 = $100,000

- Q3 2019 = $100,000

- Q4 2019 = $100,000

- Q2 2020 = $45,000

- Q3 2020 = $81,000

- Q4 2020 = $81,000

- ERC for this quarter

- ERC for this quarter

- No ERC for this quarter

In Example 2, the business suffered more than 50% revenue decline in the second quarter, so it is eligible for the ERC in the second quarter. This also means it is automatically eligible for the third quarter ERC. However, because the third quarter revenues declined by only 19%, the business will not be able to claim the ERC for the fourth quarter. This is even though the fourth quarter revenues were the same as the third quarter.

UPDATED ON 02/26/2021

4. Which Employees Can a Business claim the ERC for?

If you are a “small employer,” the ERC can be claimed on ALL employee wages (see employee wage limits in Question #6 below, and subject to family restrictions described next). See Question #5 for a further description of a “small employer.”

If you are not a small employer, the ERC can ONLY be claimed on wages paid to employees for not working. The definition of employees “not working” should be carefully reviewed with your professional advisors. Additional guidance is necessary to determine if employees are considered “not working” for purposes of their wages being eligible for the ERC.

Wages paid to certain related parties and owners are limited (under rules similar to Section 51(i)). Family members such as siblings, children, parents, grandparents, etc. are ineligible for this credit. IRS FAQ #59 lists the ineligible relationships:

- A child or a descendant of a child;

- A brother, sister, stepbrother or stepsister;

- The father or mother or an ancestor of either;

- A stepfather or stepmother;

- A niece or nephew;

- An aunt or uncle;

- A son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law or sister-in-law.

Ineligible wages also include wages paid to an employee with an ineligible relationship (described in the link above) to someone considered to indirectly own 50% or more of the business through a constructive ownership (under §267(c)). Spouses, brothers, sisters, ancestors and descendants are considered to have indirect ownership. Indirect ownership can also occur from ownership in other business entities such as corporations, partnerships and trusts.

The self-employment earnings of self-employed individuals are not considered qualified wages.

5. What is a “Small Employer” for ERC Purposes?

A small employer is defined as have 100 or fewer full-time equivalents (FTE) when claiming the 2020 ERC. A small employer is defined as having 500 or fewer FTEs in order to claim the 2021 ERC. In both cases, the reference period is 2019 employment. In other words, for 2021 ERC, the reference period is NOT 2020 FTEs. Affiliation rules also must be analyzed in computing the FTEs.

The specific rules for computing FTEs are provided under Section 4980H (enacted in 2010 as part of the Affordable Care Act (ACA)). A full-time employee for any calendar month is an employee, who has on average at least 30 hours of service per week during the calendar month or at least 130 hours of service during that month. See this link for more information.

6. What Amount of Wages are Eligible for the ERC?

This is generally gross wages plus employer health insurance costs. The maximum qualified wages are $10,000 per year, per employee for 2020 and $10,000 per quarter, per employee for 2021.

Previously under the CARES Act, if an employer obtained a PPP loan, it could not benefit from the ERC employee at all. The CAA law changed this rule retroactively for 2020 and 2021 to require both PPP and ERC not be used on the exact same wages. Therefore, wages claimed on the PPP loan cannot be claimed for ERC.

Similarly, wages claimed for emergency paid sick leave and emergency paid family and medical leave under the Families First Coronavirus Response Act (FFCRA) are not qualified wages.

Wages and health insurance benefits claimed to generate the ERC cannot be claimed to generate certain other credits.

Section 41 – Research & Development Credit

Section 51 – Work Opportunity Tax Credit

Section 45A – Indian Employment Credit

Section 45P – Employer Wage Credit for Active Duty Members

Section 45S – Employer Credit for Paid Family and Medical Leave

Section 1396 – Empowerment Zone Employment Credit

7. What if I Obtained a PPP Loan for 2020 and I Determine I’m Also Eligible for ERC?

We are waiting on more IRS guidance on the interaction of PPP and ERC, particularly when a business has already applied for PPP loan forgiveness. If you have not filed your PPP forgiveness form, you should reconsider the amounts claimed on the form. If you filed the forgiveness form already, more guidance is needed.

It is possible that a business claimed all wages on the PPP forgiveness form despite having other expenses such as rent, interest, and utilities that could have been used. If other non-wage expenses were not reflected on the forgiveness form, does this mean these expenses could free up wages for PPP? Many times, there were more than enough wages claimed on the PPP form to support 100% forgiveness. For example, a PPP loan was obtained for $250,000, yet $400,000 of wages were claimed on the form. It is not clear whether the excess $150,000 could be used as employee retention credit wages. Moreover, it is not clear how this use of excess wages could impact the PPP headcount reduction computation.

8. What is the Amount of ERC that can be Earned Each Year?

For 2020, the credit amount is 50% of qualified wages up to $10,000. This includes the entire year. Thus, for 2020, the maximum credit per employee is $5,000 ($10,000 @ 50%).

For 2021, the credit amount is 70% of qualified wages up to $10,000 per quarter. An important difference here is that for 2021, the credit is limited to 70% of qualified wages each calendar quarter and only applies to the first two calendar quarters ending June 30, 2021. Thus, for 2021, the maximum credit per employee is $14,000. The 2021 ERC expires on June 30, 2021.

9. How is this ERC Claimed?

The ERC is not an income tax credit; instead it is a payroll tax credit and is ultimately reflected on Form 941.

Employers can access the ERC by computing their ERC for a pay period and adjusting the required tax deposit downward by the credit amount. Prior to filing Form 941, employers that have an ERC in excess of their required deposit can request an advance by filing Form 7200 (Advance Credit Form). A special provision in the CARES act indicates that penalties for failure to make a deposit of employment taxes will be waived if the employer is determined to have a reasonable expectation of the employee retention credit.

If eligibility for the ERC is determined after the quarter-end but prior to filing Form 941, the credit can be claimed on the form, per Form 941 instructions.

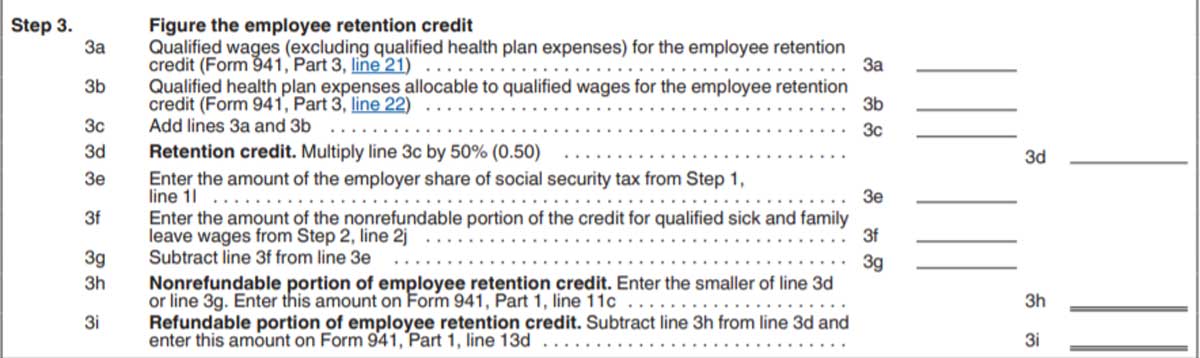

The ERC is reported on line 11c of Form 941 and, if applicable, line 13d. Qualified wages (excluding health expense) are reported on line 21, and eligible ERC wages are still reported on line 5a (Social Security wages) and line 5c (Medicare wages). Health care expenses are reported on line 22. See Worksheet 1, Step 3 of Form 941.

Finally, for 2021, a business with 500 or fewer FTEs can claim an advance credit based on 70% of the average quarterly wages for 2019. Further IRS guidance is needed for this 70% advance.

10. How is the ERC Claimed for a Quarter in Which the Business has Already Filed Form 941?

The credit can be claimed on the fourth quarter payroll tax return even if the qualified wages were paid from January 1, 2020 to September 30, 2020. We are waiting on further guidance for the mechanics of this and hope that guidance will be issued prior to the February 1, 2021 deadline to file Form 941.

Alternatively, amended payroll tax returns can be filed on Form 941-X. The instructions to Form 941-X indicate that lines 18, 26, 30, and 31 are impacted. Generally, you may correct overreported taxes on a previously filed Form 941 within three years of the date Form 941 was filed or within two years from the date you paid the tax reported on Form 941 – whichever is later according to the IRS. It is likely that most eligible employers will have to file an amended Form 941 due to the timeline.

11. Is this Credit Taxable?

Yes, the ERC credit is subject to income tax. Wages on the claimed credit must be reduced by the amount of the credit, which results in the credit being taxable income. The reduction in wages may also impact Section 199A eligible wages for purposes of the 20% qualified business income deduction. If the credit is claimed on 2020 payroll taxes after the income tax return has been filed, an amended income tax return may be required to accurately exclude wages reduced for the employee retention credit. For passthrough entities, owners’ returns will also need to be amended.

12. What are the Next Steps for Determining your Potential 2020 ERC?

Remember the maximum credit to earn for 2020 is $5,000 per employee. Secondly, note that if you have a revenue decline of more than 50% in any quarter, you will have a minimum of six months of 2020 in which you can earn ERC.

Step 1. First, determine if you meet the criteria for a significant drop in revenue of more than 50% in any quarter or meet the standard of having incurred a full or partial suspension of operations. The revenue decrease test is much more of a bright line test – meeting the standard of a full or partial suspension is subject to much interpretation and is limited only to the time frame in which the suspension was determined to be in effect.

Step 2. For employers that have 100 or fewer FTEs, here are recommended next steps:

- If you did not file your PPP loan forgiveness application, consider what wages and health insurance benefits are eligible for the ERC, and consider applying those eligible expenses to the ERC and amending Form 941.

- If you did file your PPP loan forgiveness application, consider what wages and health insurance benefits were not reported. These may be eligible for ERC. More guidance should be coming.

Step 3. For employers that are over 100 FTEs, consider what wages and benefits are eligible:

- Health insurance benefits paid for employees not working.

- Employees providing services on a part-time or full-time basis, different than what they performed prior to the pandemic, as well as employees simply not working but continuing to receive wages should be reviewed for eligibility. Consult with your advisors to determine if these identified employees meet the standard of “not working,” allowing their wages and health insurance benefits to be eligible for ERC.

As noted above, there are several areas in which IRS guidance is still needed for ERC. We address one of them in a separate article: the partial suspension criteria. Congressional intent is not well documented on this point, and legal counsel should be sought to establish a reasonable basis for any interpretations made that are not supported by authoritative guidance. There will likely be other ERC questions that surface, so stay tuned for future Sikich updates on this incentive. Please contact your Sikich advisor for any questions or ERC assistance.

Decision Tree References:

Employee Retention Credit: Main Link to IRS FAQs

Affiliated Group Rules Link: IRS FAQ

Test 1 Full or Partial Suspension Link: IRS FAQ

Test 2 Significant Decline in Gross Receipts Link: IRS FAQ

Related Party Rules Link: IRS FAQ #59

Decision tree chart is subject to change. FAQs have not been updated by the IRS for changes made to the ERC in December 2020.

This publication contains general information only and Sikich is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or any other professional advice or services. This publication is not a substitute for such professional advice or services, nor should you use it as a basis for any decision, action or omission that may affect you or your business. Before making any decision, taking any action or omitting an action that may affect you or your business, you should consult a qualified professional advisor. In addition, this publication may contain certain content generated by an artificial intelligence (AI) language model. You acknowledge that Sikich shall not be responsible for any loss sustained by you or any person who relies on this publication.