Executive summary

Healthcare M&A activity in Q1 2026 indicates a transition from cyclical recovery toward more structurally driven consolidation, supported by improving capital markets conditions and renewed institutional investor confidence.

The market is rebounding selectively, characterized by:

- A pickup in private equity (PE) and strategic deal activity across healthcare services and biopharma subsectors

- Continued strength in HealthTech, healthcare IT (HCIT), and AI-enabled platforms

- Increasing concentration of capital in higher-quality assets

- Rising deal value despite moderate volume, reflecting a shift toward larger transactions and platform investments

- AI increasingly influencing valuation in acquisition strategy

- Exit activity beginning to recover across both M&A and IPO channels, though markets remain selective

- A return to more active PE deployment, with a focus on platform consolidation and tuck-on acquisitions

Macroeconomic and capital markets context

Entering 2026, several macroeconomic factors are supporting increased transaction activity:

- Stabilizing interest rates and selective rate cuts are improving financing conditions.

- PE firms are shifting from capital preservation to active deployment.

- Healthcare continues to attract investment due to sector fundamentals, including cost inflation in care delivery, provider fragmentation, and strong services and software recurring revenue models.

These conditions are contributing to a recovery in healthcare services and HCIT deal activity, alongside an improvement in exit opportunities. While the IPO market remains constrained, strategic buyers are re-entering the market with stronger balance sheets.

Q1 2026 deal activity landscape

Market structure shift

Transaction activity continues to move from high volumes of smaller deals toward fewer, larger transactions and strategic roll-ups, as investors and corporates prioritize scale, integration, and long-term value creation. In parallel, deal structures are becoming more complex, with more minority investments, structured earnouts, and add-on acquisition strategies to manage risk and enhance return.

Capital deployment trend

Both PE and strategic buyers are increasingly focusing on:

- Efficiency and margin expansion

- Data and AI integration layers

Investors are concentrating on high-quality, scalable assets over distressed and opportunistic transactions.

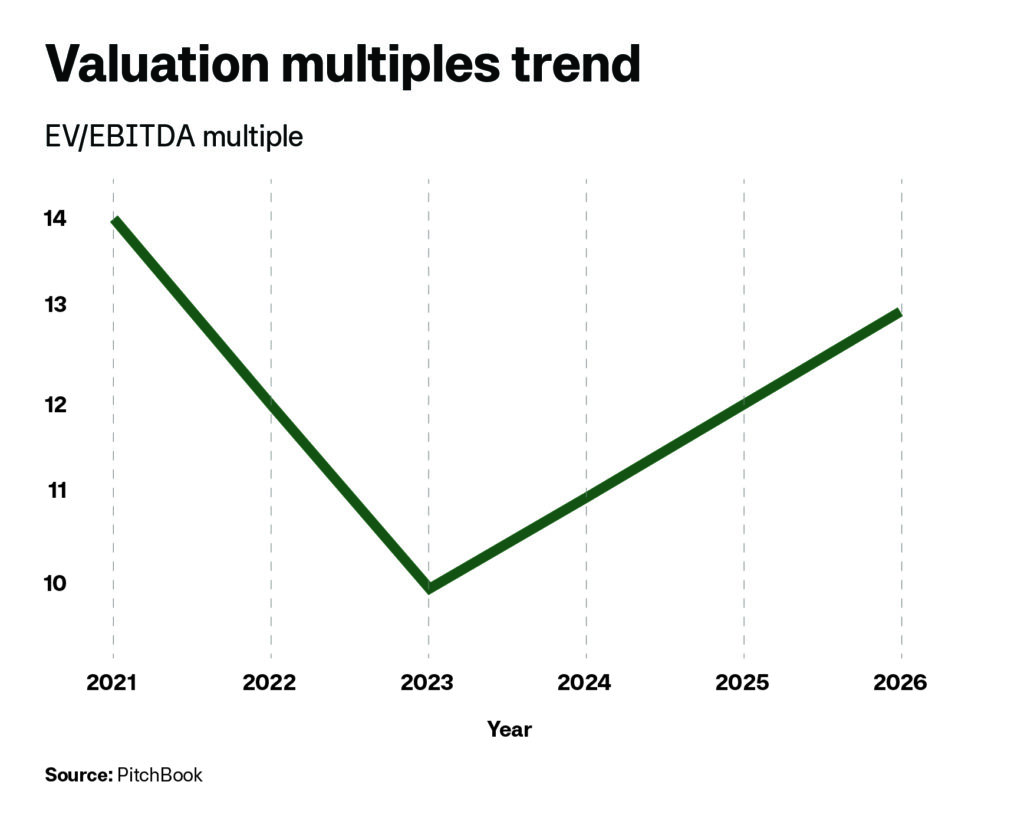

Valuation trends

Valuations are stabilizing following the 2022–2023 compression cycle, with a clearer distinction emerging between premium and discounted assets. Companies with AI integration, recurring revenue models, and strong data ownership and interoperability are increasingly commanding valuation premiums. Labor-intensive, non-digitized service models and highly regulated subsegments continue to trade at discounts.A fundamental shift in value creation is underway. Technology leverage and operational scalability are primarily driving value, rather than just traditional growth.

2026 market outlook

Deal value should continue rising as the market shifts toward fewer, larger, high-quality transactions. Overall volume will likely remain stable or grow modestly, indicating that there won’t be a broad-based recovery in activity.

Strategic consolidation should accelerate, particularly in fragmented subsectors, as corporates and sponsors expand scale and capabilities. PE deployment is also expected to increase, driven by pressure to put capital to work amid improving financing conditions.

Key drivers

Several structural tailwinds are expected to shape activity in 2026. Adoption of AI and technology-enabled solutions should drive both operational efficiency and targeted investment, particularly in data-driven and automation-focused segments.

Demographic trends, including aging populations, will continue sustaining demand across healthcare services. Ongoing market fragmentation should support consolidation strategies, especially for scaled platforms pursuing add-on acquisitions.

Improving financing conditions are expected to enhance deal activity and execution flexibility.

Risk factors

Despite positive momentum, risks remain. Regulatory scrutiny, particularly around private equity ownership, may impact deal execution and structure. Labor cost inflation continues to pressure margins, while reimbursement constraints in government programs add challenges. Geopolitical dynamics and tariff uncertainty also remain key considerations, especially for MedTech supply chains.

Strategic implications

Investors should prioritize platform-building, focusing on AI-enabled operating leverage and fragmented sectors with consolidation potential. For operators, digital transformation is now a baseline expectation, with data infrastructure being a key differentiator. Sustained margin expansion will depend on automation and scale.

Key themes

AI-driven healthcare consolidation

AI will likely be a primary driver of deal flow. Key areas of focus include:

- AI-enabled clinical tools

- Revenue cycle automation

- Diagnostics and decision support systems

Buyers are prioritizing tuck-in acquisitions that enhance data and AI capabilities to strengthen platform defensibility. They no longer view AI as a standalone vertical, but rather a valuation multiplier across all healthcare subsectors.

Rebound in healthcare services and biopharma M&A

Activity in these subsectors is expected to rebound. Forecasts point to a reacceleration in biopharma venture capital (VC) and exit activity, alongside increased strategic M&A by large pharma companies.[i] Acquisition focus areas include:

- Novel modalities such as cell and gene therapy

- Oncology and immunology pipelines

This expected rebound is being driven by ongoing patent cliffs, pipeline replenishment needs, and improving financing conditions.

HCIT and HealthTech convergence

The convergence of HCIT platforms, VC-backed HealthTech companies, and PE-backed consolidation vehicles is expected to continue. This is driving increased acquisition of VC-backed HealthTech companies by PE-backed HCIT platforms.

The sector is shifting toward platform ecosystems rather than point solutions.

MedTech expansion and strategic tuck-ins

The MedTech sector is expected to rebound, driven by innovation in cardiovascular technologies, orthopedics, surgical robots, and AI navigation tools.

Strategic acquirers are focusing on targeted tuck-in acquisitions of AI-enhanced and precision medicine assets.

PE-led consolidation of fragmented provider markets

Healthcare services remain highly fragmented, and PE firms are expected to continue executing roll-up strategies in:

- Physician practice management

- Behavioral health

- Post-acute care

- Ambulatory surgery centers

[i] PitchBook, 2026 Healthcare Outlook.

This publication contains general information only and Sikich is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or any other professional advice or services. This publication is not a substitute for such professional advice or services, nor should you use it as a basis for any decision, action or omission that may affect you or your business. Before making any decision, taking any action or omitting an action that may affect you or your business, you should consult a qualified professional advisor. In addition, this publication may contain certain content generated by an artificial intelligence (AI) language model. You acknowledge that Sikich shall not be responsible for any loss sustained by you or any person who relies on this publication.