Key takeaways:

- Q1 revealed a more cautious and uneven market than expected, despite the anticipated shift toward M&A-driven issuance.

- Overall issuance declined sharply, led by a drop in refinancings and repricings, while new-money activity remained relatively resilient.

- M&A issuance was strong but highly concentrated and partly driven by prior-year deal pipelines, with underlying private equity activity slowing.

- Credit conditions tightened as spreads widened and investor demand weakened.

- Market access favored higher-quality borrowers, with growing pressure on lower-rated credits and increasing divergence expected to persist.

U.S. leveraged loan and private credit markets

The U.S. leveraged loan market entered 2026 expecting a transition from refinancing driven activity to M&A-led issuance. While that transition is underway, first quarter results underscore a more uneven and cautious market than anticipated, shaped by macroeconomic uncertainty, sector specific stress, and widening credit dispersion.

Market activity and issuance trends

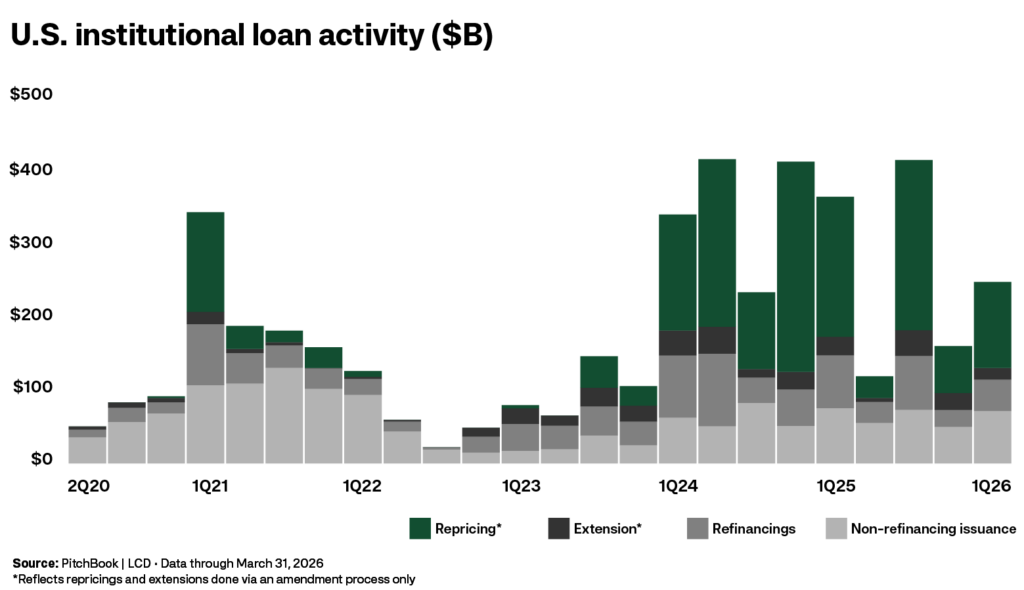

Overall leveraged loan issuance declined meaningfully in Q1. Total primary activity, including repricings, reached approximately $241 billion, running 32% below last year’s pace. The weakness was concentrated in refinancings and repricings, which fell sharply as the repricing cycle largely exhausted itself and volatility reduced borrower opportunism.

Net new issuance held up better. At roughly $70 billion, new-money issuance was only modestly below prior year levels and exceeded the quarterly average of the previous two years, indicating that deal driven financing remains viable despite softer headline volumes.

M&A‑driven issuance: strength with caveats

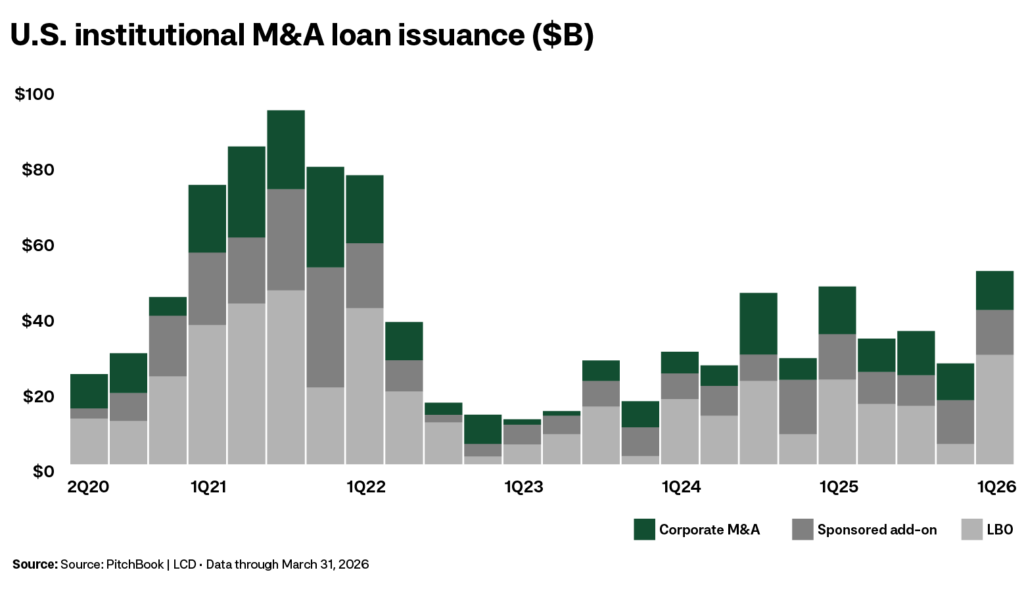

M&A-related broadly syndicated loan issuance was a relative bright spot. Buyout and corporate acquisition financing reached its highest first-quarter total since Q1 2022, marking the strongest opening quarter since the Federal Reserve began raising rates. However, this strength was highly concentrated. More than 40% of institutional loan volume came from just five mega transactions, reflecting deal concentration rather than broad based momentum. In addition, many of these transactions originated from deals announced in late 2025, suggesting that Q1 issuance benefited from pipeline carryover rather than a reacceleration of new deal formation.

Private equity deal activity slowed meaningfully during the quarter, pointing to potential headwinds for sustained M&A-driven issuance in coming quarters.

Pricing, demand, and market technicals

Market access remained available, but at a higher cost. Loan spreads widened materially in February and March, reversing the favorable pricing conditions seen in January. The most active segment of the market saw spreads widen by approximately 100 bps, reflecting heightened risk aversion tied to software sector stress, geopolitics, and a shifting rate outlook.

Investor demand weakened notably. Measurable loan demand fell to a three year low as retail fund outflows accelerated. CLO issuance remained relatively resilient but was insufficient to offset the broader pullback in demand.

Credit quality and divergence

Higher quality borrowers continued to access the market, while lower rated issuers faced widening spreads and fewer refinancing opportunities. Borrowers rated BB or higher represented a growing share of issuance, while the lowest rated segment accounted for a historically small portion of M&A-related volume.

Refinancing progress against upcoming maturities slowed meaningfully, particularly for lower rated credits. As a result, maturity pressure is becoming increasingly concentrated among weaker borrowers with limited near-term relief options.

Outlook

The first quarter highlighted a market that is open but selective. While M&A-related financing remains a source of issuance, activity is uneven and increasingly concentrated in higher quality credits and marquee transactions. Widening spreads, weaker demand, and slowing deal formation suggest that credit conditions will remain tight in the near term, with continued divergence between stronger and weaker borrowers.

Our Q4 2025 credit market update can be found here.

About our authors

Mike Rudolph is a Managing Director at Sikich Corporate Finance. He has nearly 25 years of experience orchestrating senior debt (cash flow and asset-based), junior capital, and equity financings for leveraged buyouts, recapitalizations, private placements, and balance sheet restructurings. Mike.rudolph@sikich.com

Doug Christensen is a Director at Sikich Corporate Finance. He provides capital structure advisory and capital raising support for private clients, with expertise across senior debt, junior capital and equity financing. Doug.christensen@sikich.com

Securities offered through Sikich Corporate Finance LLC, member FINRA/SIPC

This publication contains general information only and Sikich is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or any other professional advice or services. This publication is not a substitute for such professional advice or services, nor should you use it as a basis for any decision, action or omission that may affect you or your business. Before making any decision, taking any action or omitting an action that may affect you or your business, you should consult a qualified professional advisor. In addition, this publication may contain certain content generated by an artificial intelligence (AI) language model. You acknowledge that Sikich shall not be responsible for any loss sustained by you or any person who relies on this publication.