Under the SECURE Act 2.0, those born in or after 1951 do not need to begin taking Required Minimum Distributions (RMDs) from traditional IRAs until age 73. Prior to the Act, individuals had to start taking the RMD at age 72.

Note that IRA distributions are taxable to an individual when paid to an individual.

For tax planning purposes, if you have some of your charitable donations made directly from your IRA, rather than directly from other funds, this action could result in tax savings in 2023. With a QCD, you authorize your IRA custodian to make a distribution directly to a charity you select, rather than to you. This is an important distinction for the distribution. The QCD must go directly to the charity to qualify. Further, the QCD is treated as part of your RMD for the year.

While the SECURE Act and SECURE Act 2.0 changed the age to begin taking an RMD, the Acts did not change the age that you could begin using a QCD. The QCD is available to those over the age of 70 ½.

Tax Treatment of a QCD: You do not include the amount of the QCD paid to charity in your income. Further, you are not entitled to a charitable tax deduction for the QCD amount. You will receive a year-end Form 1099-R for the total IRA distributions, including QCD amounts. However, the taxable IRA amount on a return will not include the QCD amounts. Individuals are limited to $100,000 of QCDs in a year.

One other possible non-tax benefit with a QCD relates to individuals on Medicare. If you have a high income, the law requires an adjustment to your monthly premiums for Medicare Part B (medical insurance) and Medicare prescription drug coverage. Higher income beneficiaries pay higher premiums for Part B and prescription drug coverage.

This affects less than 5% of individuals with Medicare, so most people do not pay a higher premium. If your adjusted gross income (AGI) is above $194,000 for 2023 using the married filing jointly status, your Medicare premiums are increased (the tier for 2024 is not yet set but is expected to be approximately $205,000).

Depending on your situation, and since the amount of a QCD is not included in your AGI, using a QCD might keep your Medicare premiums from being increased. Click here to view the Social Security website’s explanation of this adjustment (please note these thresholds and premiums are adjusted each year).

Using this QCD approach, you direct your IRA custodian to send a check to your favorite not-for-profit as either a one-time donation or a monthly payment, depending on your preference. Some IRA custodians now provide their clients with an IRA checkbook, rather than having to contact the custodian each time.

At the end of the year, you will receive a Form 1099-R for the full amount of your IRA distributions. You will need to let your accountant know what QCD amounts you made from your IRA, as your tax return will reflect the gross amount received (QCDs are subtracted to arrive at the net taxable amount). You will also need a charitable acknowledgement of the QCD amount from the charity.

One important caveat is the charity cannot provide you with any goods or services in exchange for the QCD. This includes state tax credits. If making a charitable contribution that provides you with a state tax credit, such contribution should be made from your after-tax funds, not an IRA.

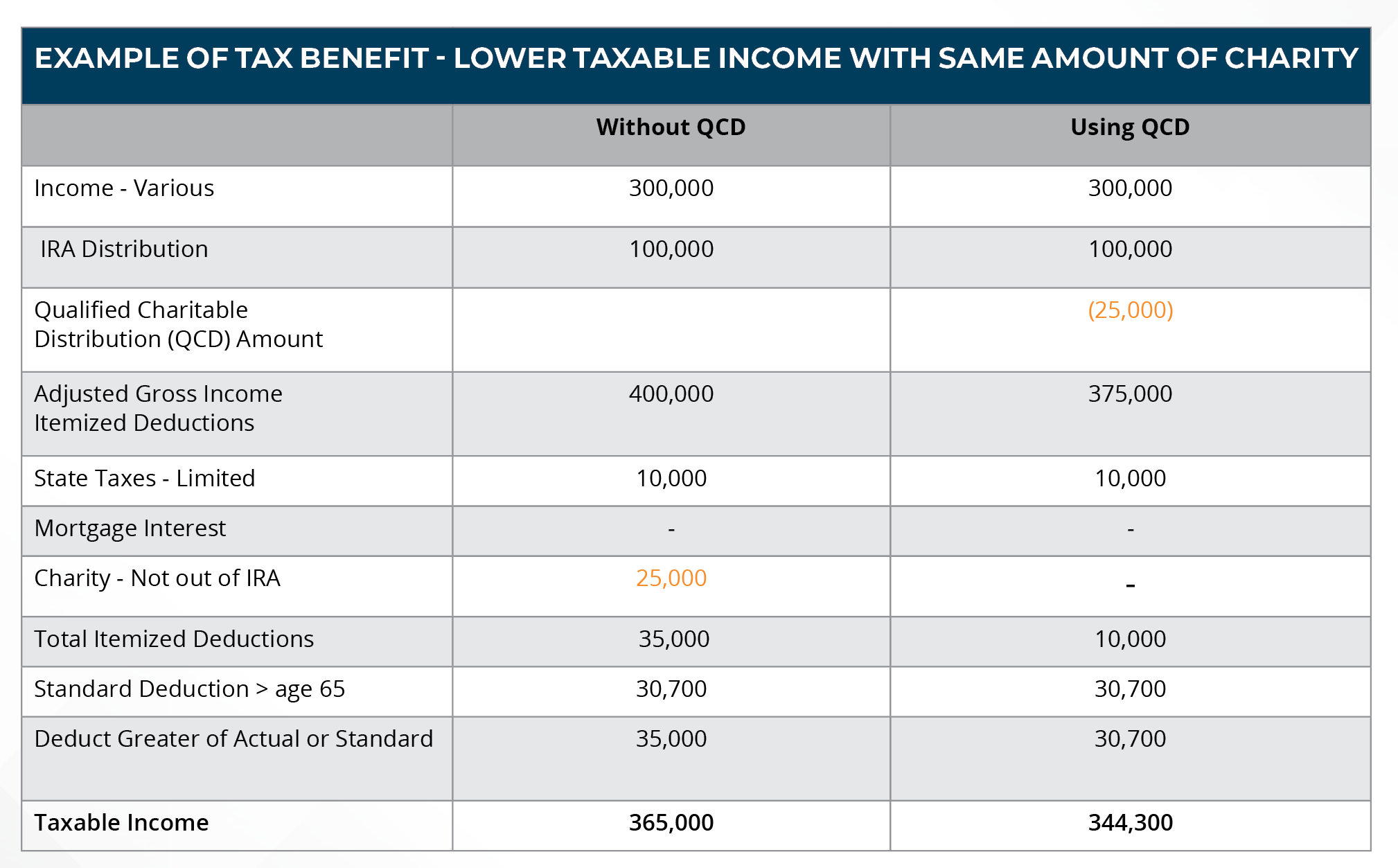

Here is an example of the tax savings when using a portion of your RMD as a QCD from your IRA:

A taxpayer has an RMD of $100,000 for the year and plans to make $25,000 in charitable contributions. Using the QCD strategy would benefit such an individual.